Logistics

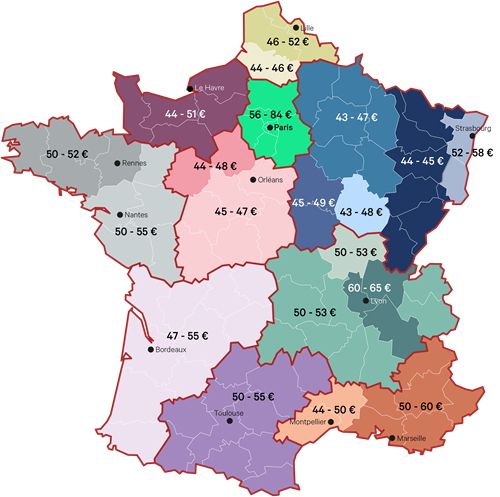

Logistics rent range – Q1 2023

April 14, 2023

This period of calm, which is known to be temporary, is taking place in a context marked by record levels of logistics rents. More than ever, the question of the sustainability of such rental values for users arises.

Moreover, this brake could have led to a possible lull in the growth of logistics rents. At the end of the first quarter of the year, this was not the case.

The increase has never been so clear-cut and significant as in the tensest historical sectors: Lyon and Marseille. In Lyon & satellites (St Quentin Fallavier, Pont d'Ain) prime rent has reached €65 (+8% over three months) regardless of whether it is a new or second-hand asset, illustrating the imbalance between very strong demand and almost zero supply for these highly sought-after locations. The rise is also palpable in the rest of the region, although there is still a dichotomy depending on the quality of the asset.

In Marseille, rents are following the same trend: due to a lack of vacant and future supply, new and second hand properties are lining up at €60 for the upper range, although the spread between the minimum and maximum is still significant.

In the South-West, after having risen sharply at the end of 2022, rents are holding steady at the beginning of this year due to a lack of significant transactions and supply on the market, although it is likely that these levels have not yet reached their maximum.

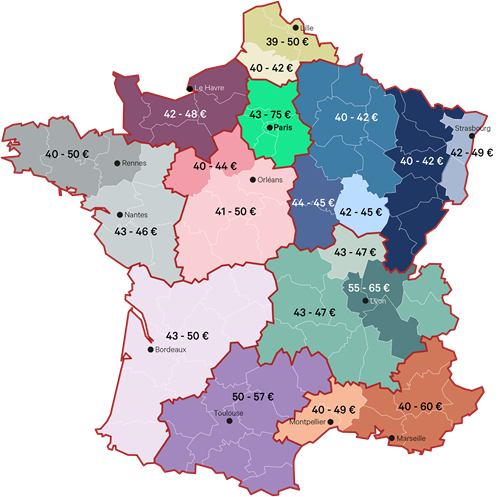

However, the lack of supply is not the only factor boosting rents. In the Nord-Pas-de-Calais region, where current and future logistics reserves are the most substantial, prime rent for new products has risen from €49 to €52 and to €50 for second-hand products.

Another aspect that is pushing up rents for new products is the rise in the cost of money and construction costs, which inevitably has an impact on the necessary levels that rental values must reach to allow developers' balance sheets to turn around.

This continued rise in rents even in a downturn continues to raise questions. How will users be able to adapt? Will they be forced to locate in still emerging locations? Will they abort their decision to expand?

Logistics Rent map

Second- hand logistics rent map

From 12 April, you can find our full Q1 review here: https://www.cbre.fr/insights#analyses-de-march%C3%A9

Insights in Your Inbox

Sign up for our Newsletter